Vocabulary

- think about: To consider something carefully.

- have to: Must do

- look at: To use your eyes to focus on something

- over to: Used to hand over to someone else to speak

- in the future: At a later time; in times to come.

- for example: As an illustration or instance.

- as well as: Also; in addition to

- rather than: More exactly; more correctly

- on the line: At risk; in a situation where something could be lost.

- lead to: To result in some action

- such as: For example; like

- in general: Typically; usually; on the whole.

- put off: To take off, e.g. clothing

- talking about: To discuss a particular topic.

- in a bubble: Living isolated from reality or outside events.

- think of: To look on as (being something specific); consider

- in fact: Used to emphasize the truth of a statement, especially one that contrasts with or contradicts something else.

- of course: Sure ; Certainly

- opt in: To choose to participate in something; to give explicit consent.

- over time: Gradually; as time passes.

- study for: To prepare for an examination or test by learning and revising the subject matter.

- follow through: To fulfill a promise

- based on: To use something as the foundation or starting point for something else.

- set up

- show up: To arrive or be seen at a place, e.g. a party

- from the top: From the beginning.

- thankful for: Feeling or expressing gratitude; appreciative.

- at risk: In danger; likely to be harmed

- connected with: Related to; associated with.

- out there: In or to a place that is far away

- bad habits: Negative or harmful routines or behaviors that are difficult to stop.

- in a nutshell: As a summary; including the main points concisely

- at work: Located at one's place of employment

- under the assumption: Based on the belief or supposition that something is true.

- future self: The person you will become in the future, often used in the context of making decisions that will benefit your future well-being.

- in mind: Being aware of or considering something.

- rule of thumb: A practical and approximate way of doing or measuring something.

- spend money: To use money to buy or pay for something.

- fill out: To become fatter

- get around to: To finally start doing something you avoided doing

- at the same time: Simultaneously; at the identical moment.

- same time: Occurring simultaneously or at the same point in time.

- point out: To make others aware of an idea

- work at: To have a job at a particular place or organization.

- the following: Next in order or sequence.

- from the first: From the very beginning.

- for sure: Definitely; certainly; without a doubt.

- of interest: Relevant or important to someone or something.

- figure out: To understand the behavior of someone

- know about: To have information or understanding of a subject or situation.

- for the better: Resulting in improvement; to a more favorable condition.

- sign up to: To register for something, like a service or a course.

- regardless of

- paying off: To give money to get person to do something; bribe

- rely on: To depend on someone or something

- work in: To make an opening for something in your schedule

- pile up: To put things on top of each other to form a pile

- interact with

- result in: To cause or produce as a consequence.

- in the long run: Eventually; over a long period of time.

- through with: Having had enough (of trouble); wanting to stop

- pay up: To pay money that you owe

- put together: To build or assemble something small, e.g. a toy

- in particular: Specifically; especially.

- on a day-to-day basis: Happening regularly every day as a routine.

- as a gift: Given without expectation of payment; a present.

- on the other hand : Considering a different aspect of the matter; alternatively.

- face to face: (Meeting) while looking at someone

- come by: To become the owner of something, e.g. by accident

- in line with: In agreement with; conforming to.

- in with: Fashionable or popular at the moment.

- come up to: To meet expectations

- out of time: Having no more time available to do something.

- to do with: To be about something; concern

- in agreement: Sharing the same opinion or feeling.

- thanks to: Because of; as a result of.

- phone number: A sequence of digits assigned to a telephone subscriber, used to make a call to that phone.

- people: Persons sharing culture, country, background, etc.

- commitment: Permanent love or concern for person, thing

- decision: Choice made after thinking; final judgment

- security: Department in a company in charge of protection

- information: Collection of facts and details about something

- behavior: The way a person or thing acts; manner

- today: This day; day that is happening now

- financial: Involving money

- bound: To cover a wound, as with a bandage

- group: Two or more musicians who play music together

- incentive: Something that encourages you to do something

- default: Automatic setting when no indicated preference

- program: To make someone act or think in a certain way

- economic: Concerning trade, industry, and money

- participate: To take part with others in doing something

Get the full experience in the app

Learn anywhere with detailed sentence and usage analysis

01:03

She took a brave step forward, leaving behind her comfort zone to chase her dreams.

Vocabulary

- brave

adj. Having courage

- comfort zone

phr. A familiar situation where one feels safe

Explanation

a brave step is a noun phrase, where brave is an adjective modifying the noun step, meaning "a courageous step".

forward is an adverb modifying step, meaning "ahead".

The whole phrase serves as the object, answering the "what" of took (verb) — she took a brave step forward.

Get the full experience in the app

Look up words anytime with pronunciation, part of speech, and usage

brave

US/brev/

UK/breɪv/

adj.Brave

v.t.To bravely face

A2 Elementary

Get the full experience in the app

Practice speaking anytime and get instant pronunciation feedback

Try this speaking exercise.

Try practicing with this sentence.

80

WEBINAR: Behavior Economics 101

0

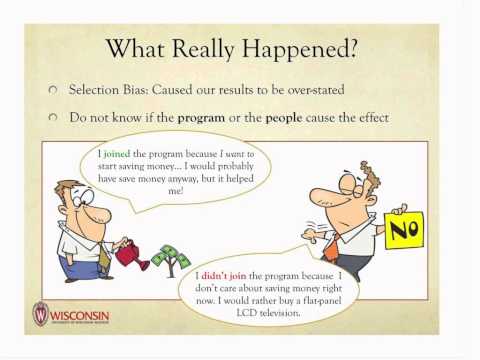

FlashJack posted on 2015/01/11Ever wonder why we make certain financial decisions? This webinar dives into the fascinating world of Behavioral Economics, showing you how 'default nudges' and 'commitment devices' can actually help us save more and spend smarter! You'll pick up practical vocabulary for everyday financial discussions and workplace scenarios.

Learn this video on the APP!

The VoiceTube App has more in-depth practice for videos!