Subtitles & vocabulary

60 Second Adventures in Economics combined - CAPTIONED

0

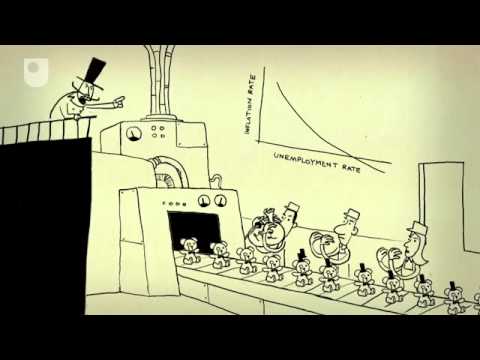

Eating posted on 2024/05/10Ever wondered how the 'Invisible Hand' actually works or why saving too much might be bad? This super-fast video breaks down fascinating economics concepts like the Paradox of Thrift and Comparative Advantage in just 60 seconds! You'll pick up some awesome vocabulary and get a clearer picture of how the world's economy ticks.

Video vocabulary

advantage

US /ædˈvæntɪdʒ/

・

UK /əd'vɑ:ntɪdʒ/

- Noun (Countable/Uncountable)

- Thing making the chance of success higher

- A positive point about something

- Transitive Verb

- To make use of something, especially to further one's own position; exploit.

A2TOEIC

More spot

US /spɑt/

・

UK /spɒt/

- Noun

- A certain place or area

- A difficult time; awkward situation

- Transitive Verb

- To see someone or something by chance

A2TOEIC

More demand

US /dɪˈmænd/

・

UK /dɪ'mɑ:nd/

- Noun (Countable/Uncountable)

- Desire customers have to buy product, service

- A strong request for someone to do something

- Transitive Verb

- To strongly request someone to do something

- To need something.

A2TOEIC

More rational

US /ˈræʃənəl/

・

UK /'ræʃnəl/

- Adjective

- Able to think clearly

- A real number that can be written as a ratio of two integers.

- Noun

- A rational person.

A2TOEIC

More Use Energy

Unlock Vocabulary

Unlock pronunciation, explanations, and filters